Can Thinking About How We Think Make Us Better Investors?

As humans, most of us have biases and cognitive errors that can play a role in our investment decision-making, but we also have the unique ability to analyze our own thoughts.

The psychological phenomenon that leads to anomalies and inefficiencies in the market, such as the tendency to overreact to bad news (De Bondt and Thaler), and momentum trending (Jegadeesh and Titman) may create opportunities for outperformance. Behavioral finance attempts to understand the divergence between what rational models of economics and finance predict and what actually occurs, by observing how investors behave. Recognizing certain psychological tendencies can help us avoid common errors in judgment that may put achieving your financial goals at risk. To explore this, we’ll take a closer look at a few of these common proclivities:

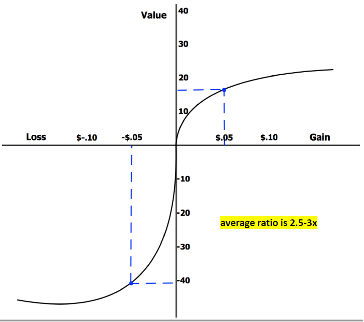

- Loss Aversion – a logical approach to risk would mean that given two options with identical expected values, a person would choose the option with the most certainty (least amount of risk). For example, given the choice between a 100% chance of receiving $500 or a 75% chance of receiving $500 a rational person would choose the former because it has a higher probability. This is how most people behave, but if the options are changed slightly we begin to see the introduction of a bias toward loss aversion (Kahneman and Tversky), which is the observation that people tend to feel the emotional pain of losing money more intensely than they feel the emotional satisfaction of gaining an equivalent amount of money.

Daniel Kahneman and Amos Tversky illustrate this with the following example:

Given a 50% probability of winning $150 and a 50% probability of losing $100, is an individual likely to take this gamble? The answer is no, their experiments show that most people will not take a gamble unless the possible gain is at least 2x greater than the potential loss.

Source: Kahneman, Daniel, and Amos Tversky. 1979. “Prospect Theory: An Analysis of Decision under Risk.”

- Anchoring and Adjustment – When making decisions based on new information, ideally, we would consider it objectively and update our prior beliefs without bias. It is common, however, for people to initially establish an “anchor” and then overemphasize the importance of that reference point when approximating the value of something. The subsequent information is then used to adjust the estimated value only marginally, due to an emotional attachment to the original anchor point. This can make it difficult for someone to sell an investment when the price has dropped from their initial purchase price, even when new information has justifiably lowered its value. Studies on this phenomenon have been conducted by Edward Joyce and Gary Biddle, as well as Stephen Butler and others.

- Mental Accounting – Studies by Richard Thaler have shown that people tend to treat equal amounts of money differently depending on factors such as their source or planned use. This is contradictory to the purely logical position that $1 has the same purchasing power as any other $1, and therefore money is interchangeable regardless of where it comes from. By establishing different accounts in our minds such as “bonus money”, “salary money”, “gift money”, etc. people may justify decisions that are detrimental to achieving their goals. An example could be when someone is willing to take more risk with equity bonuses and doesn’t appropriately diversify their investments. Another example is when people quickly spend their cash bonus on frivolous things because it wasn’t budgeted in a similar way as their salary.

We know that mathematical models based on logical reasoning alone do not consistently predict how the economy or stock market will perform. Using technical analysis can help identify trends in the market and capitalize on anomalies. Macro and fundamental analysis is a rigorous way of conducting due diligence and objectively incorporating relevant information into investment decision-making. This is enhanced further by being aware of our own personal biases and having an advisor who can help us recognize and avoid them.

Our investment process blends Technical, Macro, and Fundamental Analysis investment principles into a focused strategy. Contact us if you'd like help bringing all three perspectives together to take a more thorough and prudent approach resulting in deeper insights for the long term.

Kahneman, Daniel, and Amos Tversky. 1979. “Prospect Theory: An Analysis of Decision under Risk.”

Joyce, Edward G., and Gary C. Biddle. 1981. “Anchoring and Adjustment in Probabilistic Inference in Auditing.”

Butler, Stephen A. 1986. “Anchoring in the Judgmental Evaluation of Audit Samples.”

Thaler, Richard H., and Eric J. Johnson. 1990. “Gambling with the House Money and Trying to Break Even: The Effects of Prior Outcomes on Risky Choice.”