New Tax Proposals - July 2021 Update

President Biden recently announced more details on new tax proposals to fund the American Families Plan that includes expanded education, child care, paid leave, and other reforms. The proposals would raise $1.5 trillion over a decade.

While the changes are subject to debate in Congress and maybe significantly altered or fail to pass into law, below are some of the proposed key points and planning considerations for clients:

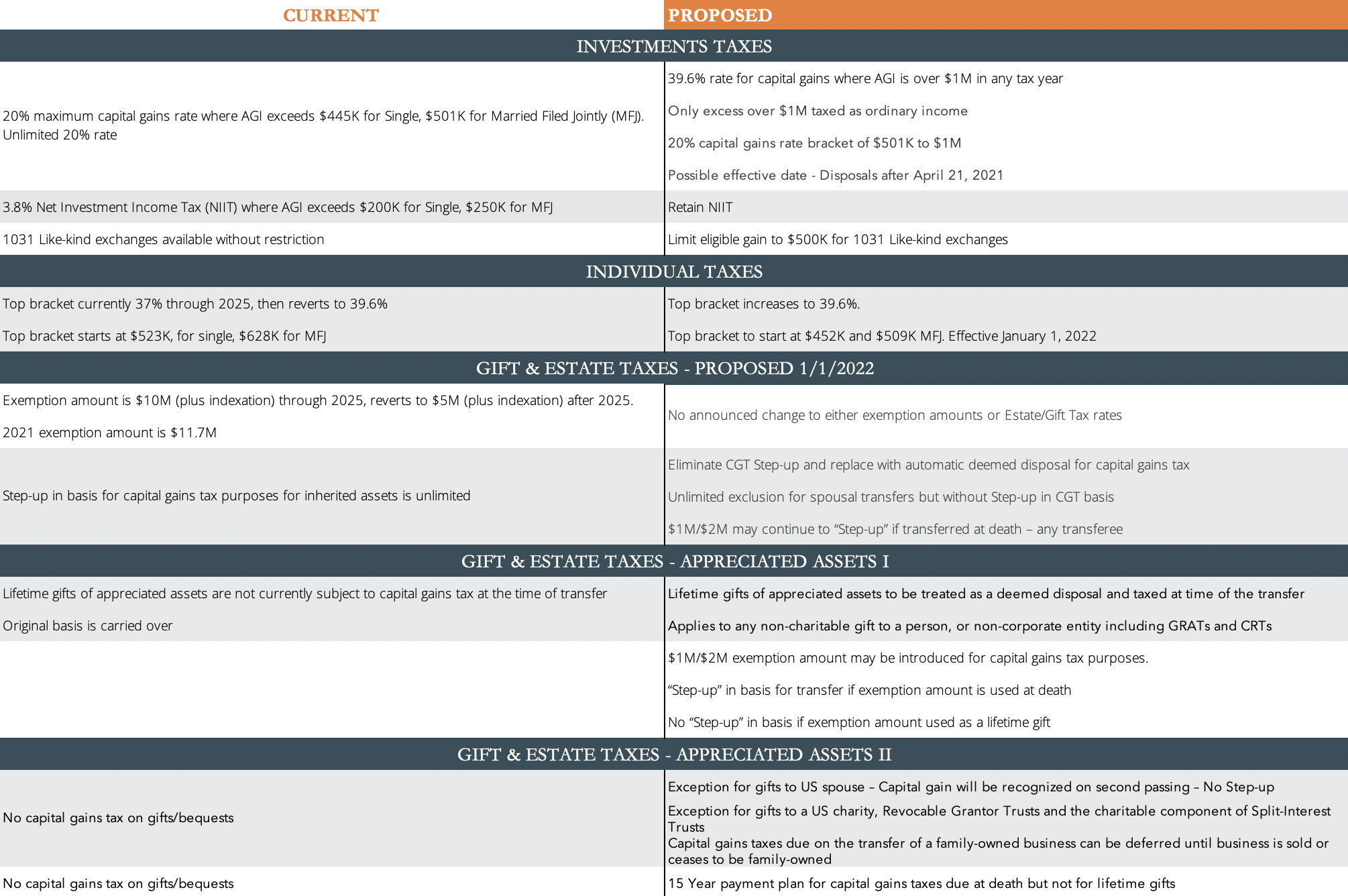

Increase in the top income tax bracket back to 39.6% and re-instate the top income tax rate of 39.6% for tax years 2022 and after.

The ordinary income thresholds at which the top rate would apply would be reduced. For Married Filing Jointly it is proposed that the top rate would apply to incomes above $509K (down from $628K for 2021) and for single filers, it would apply at $452K (down from $523K for 2021).

- Planning impact: The proposal could impact high earners, trusts that pay tax at the top marginal rate on income not distributed to beneficiaries, and taxpayers exercising non-qualified stock options (NSOs) in 2022 and after.

Increase Long-Term Capital Gains Tax to 39.6% on incomes above $1 million

The plan would increase the top tax rate on capital gains from the current 20% (plus 3.8% Net Investment Income Tax for a total of 23.8%) to 39.6% (plus 3.8% NIIT for a total 43.4%). The proposal would apply only to taxpayers with total taxable incomes of more than $1 million and would apply only to those gains which are in excess of the $1M threshold. In addition, many states also tax capital gains which could result in combined capital gains taxes of over 50%.

The Treasury recently announced that this change could apply to gains realized after April 21st, 2021 – potentially affecting the 2021 tax return year. Where taxable income is less than $1M clients will continue to benefit from the Long-Term Capital Gains tax rate of 20% plus NIIT.

- Planning impact: Limit total taxable income to under $1 million – clients need to be cognizant that gains realized after April 21, 2021 are potentially subject to the higher ordinary income tax rates where taxable income exceeds $1M in 2021. Where taxable income may exceed $1M, it may be beneficial to use charitable trusts to defer capital gains and smooth income recognition over many years, staying below the $1M limit. Make charitable contributions of appreciated assets – the tax deduction may be worth more than selling the asset and paying the tax. Charitable contributions also remove assets from a taxable estate and therefore save on estate taxes.

End of Capital Gains step-up to market value for assets owned at death

Currently, an asset’s unrealized appreciation isn’t subject to capital gains tax at death. Assets owned by the decedent transfer to heirs at the market value at the time of passing. Heirs can then sell the asset without realizing significant gains. The latest tax proposal would tax the unrealized capital appreciation of most assets owned at the time of passing even where no actual sale of the asset takes place.

There will likely be a $1 million exemption per individual ($2 million if married filing jointly) – and for family businesses where the business is passed to and carried on by the next generation. Assets using the $2M exemption amount would step up the tax basis to fair market value at death. There will also be an unlimited exemption from capital gains tax for Spousal transfers (to a US citizen spouse) at death – however, there would be no step-up in basis on such transfers (above the $2M exemption amount) and the tax realization for capital gains tax purposes would take place at the passing of the second spouse.

- Planning impact: It previously benefited taxpayers to retain assets within the taxable estate to take advantage of this big tax break. The proposal would mean there is now less downside to making lifetime gifts of assets and using the estate/gift tax exemption amount to remove assets from the taxable estate – however, See the comparison chart below: Treat lifetime gifts of appreciated assets as a realization for capital gains tax.

Treat lifetime gifts of appreciated assets as a realization for capital gains tax

Currently, an asset’s unrealized appreciation isn’t subject to capital gains tax when it is transferred by way of a gift. The proposal would treat such transfers as a deemed disposal and tax the unrealized capital appreciation of most assets even where no actual sale of the asset takes place. This proposal would apply to transfers by way of gift to individuals and most types of trusts (including Grantor Retained Annuity Trusts and split-interest charitable trusts such as Charitable Remainder Trusts and Charitable Lead Trusts). The effective date for this proposal would apply to transfers that take place after 12/31/2021.

There will likely be a $1 million exemption per individual ($2 million if married filing jointly). For family businesses, where the business is transferred to and carried on by family members, the capital gains tax would be deferred until the business was sold or was no longer a family business. There will also be an unlimited exemption from capital gains tax for lifetime Spousal transfers (to a US citizen spouse) – however, there would be no step-up in basis on the transfer and the tax realization for capital gains tax would take place at the earlier of the passing of the second spouse or when the asset was sold. There will likely be a full exemption for outright transfers to recognized charities and for transfers to Revocable (lifetime) Grantor Trusts.

- Planning impact: The proposal would only affect transfers by way of gift of appreciated assets that take place after December 31, 2021 – Consider gifts and funding of trusts in the tax year 2021 to escape the application of capital gains tax on such transfers in 2022.

Limit the tax benefits of 1031 exchanges

Currently, real estate investors can defer paying capital gains taxes on investment properties by reinvesting proceeds in a 1031 exchange property. The proposed new law would limit the deferred gain to $500,000 and immediately tax any gain in excess of that amount.

- Planning impact: Consider doing a 1031 exchange where the gain is over $500,000 before the law becomes effective.

What isn’t currently proposed to change:

- No change to estate/gift tax exemption amounts ($11.7M per taxpayer for 2021) or to the rates of these taxes.

- No removal of the SALT (state and local tax) cap deduction limitation – remains $10,000. Although this was a campaign promise, the latest proposals do not mention this change specifically.

- Introduce Social Security at 12.4% on W2 income over $400,000 – although this was a campaign promise, the latest proposals do not mention this change specifically.

While the final guidelines and timing of the legislation are to be determined, it’s prudent to begin talking to your financial advisor, tax advisor or accountant, and estate planning attorney. Contact BakerAvenue to help you review your options and to be ready to make changes as necessary.

Sources: General Explanations of the Administration’s Fiscal Year 2022 Revenue Proposal.

Sources: General Explanations of the Administration’s Fiscal Year 2022 Revenue Proposal.