New Tax Proposals - May 2021

President Biden recently announced new tax proposals to fund the American Families Plan that includes expanded education, child care, paid leave, and other reforms. The proposals would raise $1.5 trillion over a decade by taxing the highest earners.

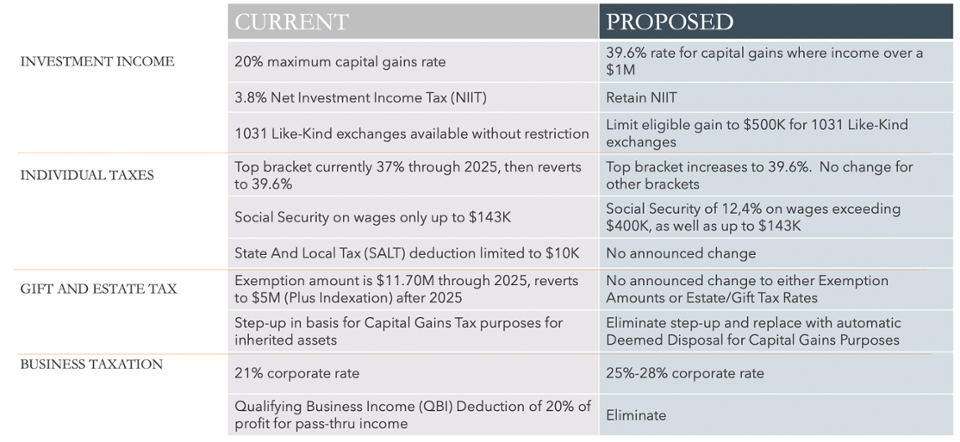

While timing and changes are subject to debate in Congress, here are some of the proposed key points and planning impact considerations:

End of Capital Gains step-up to market value for assets owned at death

Currently, an asset’s unrealized appreciation isn’t subject to Capital Gains tax at death. Assets owned by the decedent transfer to heirs at the market value at the time of passing. Heirs can then sell the asset without paying Capital Gains tax. The latest tax proposal would tax the unrealized capital appreciation at the time of passing even where no actual sale of the asset takes place.

There will likely be a $1 million exemption per individual ($2 million if married) – and also for family businesses when the business is carried on by the next generation.

- Planning impact: It previously benefited taxpayers to retain assets within the taxable estate to take advantage of this big tax break. The proposal would mean there is now no downside to making lifetime gifts of assets and using the estate/gift tax exemption amount to remove assets from the taxable estate or to simply selling the appreciated asset either during 2021 or over multiple tax years.

Increase in the top income tax bracket back to 39.6%

This is essentially accelerating the change back to the top income tax rate of 39.6%, which is scheduled to take effect after 2025. The exact income thresholds at which the rate would apply for single taxpayers and married joint filers is to be determined but would be at least $400,000.

- Planning impact: The proposal would impact high earners, trusts which pay tax on income not distributed to beneficiaries and taxpayers exercising non-qualified stock options (NSOs).

Increase Capital Gains tax to 39.6% on incomes above $1 million

The plan would increase the top tax rate on Capital Gains from the current 20% (plus 3.8% Net Investment Income Tax for a total of 23.8%) to 39.6% (plus 3.8% NIIT for a total 43.4%). The proposal would apply to taxpayers with total taxable incomes of more than $1 million. In addition, many states also tax Capital Gains which could result in combined Capital Gains taxes of over 50%.

- Planning impact: Take Capital Gains prior to the proposal becoming law. Limit total income to under $1 million after the law becomes effective, where possible. Use charitable trusts to defer capital gains and smooth income recognition over many years. Make charitable contributions of appreciated assets – the tax deduction may be worth more than selling the asset and paying the tax. Charitable contributions also remove assets from a taxable estate and therefore save on estate taxes.

Limit the tax benefits of 1031 exchanges

Currently, real estate investors can defer paying capital gains taxes on investment properties by reinvesting proceeds in a 1031 exchange property. The proposed new law would limit the deferred gain to $500,000 and immediately tax any gain in excess of that amount.

- Planning impact: Consider doing a 1031 exchange where the gain is over $500,000 before the law becomes effective.

Restrict the use of Family Limited Partnerships to discount the value of non-business assets for gift/estate tax purposes

The treasury has said that it will target the use of the FLP discount technique where non-business assets such as stock holdings and collectibles are included with regular business assets.

Introduce Social Security at 12.4% on W2 income over $400,000 (single filer)

The new tax would be split 6.2% from employee and 6.2% from employer.

- Planning impact: As well as regular high earners, those exercising non-qualified stock options (NSOs) would be impacted. Exercise NSOs before the law takes effect.

Eliminate the QBI (qualified business income) tax deduction

The QBI currently allows taxpayers who are self-employed or run a business as a pass-through entity to deduct up to 20% of their net profit in figuring their tax liability.

Increase the corporate tax from the current 21% rate to 25% - 28%

- Planning impact: This may have a short-term effect on stock prices.

What isn’t proposed to change:

- No change to estate/gift tax exemption amounts ($11.7M per taxpayer for 2021) or to the rates of these taxes.

- No removal of the SALT (state and local tax) cap deduction limitation – remains $10,000.

SUMMARY COMPARISON

Sources: Tax Foundation 2020 Capital Gains, Tax Foundation Joe Biden 2020 Tax Plan

While the final guidelines and timing of the legislation are to be determined, it’s prudent to begin talking to your financial advisor, tax advisor or accountant, and estate planning attorney. Contact BakerAvenue to help you review your options and to be ready to make changes as necessary.