How to Take Advantage of Tax-Loss Harvesting

Tax-loss harvesting is both simple and complex. On the surface, it is as simple as sell your losers and take the tax write-off. But it can also get complex, requiring an appreciation of market volatility, correlation between different stocks, and the trickier parts of the tax code as it relates to Wash Sales. In this article, we take a look at these different areas and examine those situations where proactive tax-loss harvesting can be particularly powerful.

The Winners and Losers

Every year, in every portfolio, there will be some stocks that have performed poorly. A loss of patience with poorly performing stocks can often lead investors to sell the stock and crystalize the loss for tax purposes – taking some benefit through off-setting the loss against gains elsewhere in the portfolio. What investors often fail to appreciate is that by selling the losers, they may be capturing tax benefits, but they are probably costing themselves money by exiting the losing positions. Successful tax-loss harvesting, that doesn’t hurt overall returns, requires that the proceeds be re-invested back into the area of the market that gave rise to the losing position in the first place. Not re-investing the proceeds correctly will usually leave you with plenty of tax losses but an overall below-market return.

To reiterate, the objective of tax-loss harvesting is to keep returns at, or near, those of the wider market, and to create assets, in the form of tax write-offs, along the way. The goal is to have market-based returns but with a smaller tax bill than had no tax-loss harvesting been utilized.

Taking Tax Losses: The Wash Sale Rule

For tax-loss harvesting to be successful, it is not simply enough to take the losses. Maintaining market exposure is key and sale proceeds from the losing position must be redeployed into a replacement position to maintain market exposure. This is when we must pay attention to the Wash Sale Rule. This rule prohibits losses from being taken for tax purposes where the loss position is replaced with a “substantially identical” position within 30 days, before or after, the date that the loss position is sold. The Wash Sale Rule applies to most of the investments you would hold in a typical brokerage account or IRA, including stocks, bonds, mutual funds, exchange-traded funds (ETFs), and options.

The tax loss will be disallowed if you buy the same security, a contract or option to buy the security, or a "substantially identical" security, within 30 days before or after the date you sold the loss-generating investment (a 61-day window). Many investors fail to appreciate that a loss on $10,000 of Amazon stock bought on 1st February and sold on 1st December will be disallowed if the investor:

- also bought $10,000 of Amazon stock on 15th November or

- also bought $10,000 of Amazon stock on 15th December

Additionally, you cannot get around the Wash Sale Rule by selling an investment at a loss in a taxable account, and then buying it back in a tax-advantaged account. Further, the IRS has stated it believes a stock sold by one spouse at a loss and purchased within the restricted time period by the other spouse is a wash sale.

Successful tax-loss harvesting requires that the replacement stock not be Amazon shares – it can be another stock or an index that is closely correlated to Amazon. Re-investing in a stock or index that is closely correlated to Amazon allows market exposure to be maintained and allows the investor to take the realized tax loss while not falling foul to the Wash Sale Rule disallowance.

Maintaining Market Exposure

This is important because all too often, a stock that was yesterday’s beaten down dog is, most likely, tomorrow’s rising star – selling for the tax loss is fine, but unless a similar position is re-established, the investor risks missing the rebound and will be left with a realized loss and none of the upside. Tax-loss harvesting isn’t “picking better stocks,” but rather a way of improving the post-tax performance of a given portfolio of stocks by turning, non-deductible, unrealized losses that can appear and then quickly disappear - into realized losses, which are tax deductible - but without losing market returns.

What Is Active Tax-Loss Harvesting?

Systematically selling a security that has experienced a loss

Systematically selling a security that has experienced a loss- “Harvested” losses can offset capital gains and some income

- The sold security is replaced by a similar one, maintaining similar exposure and risk characteristics of a portfolio strategy, like the S&P 500 index

- Due to IRS “wash sale” rules, the sold security cannot be bought back for 30 days

Are Some Markets Better Suited to Tax-Loss Harvesting Than Others?

Based on the above, it should be apparent that there are some “markets” that are better suited to a tax-loss harvesting strategy than others. Markets that experience high degrees of volatility with large up days and large down days will deliver many more tax-loss harvesting opportunities than markets that are becalmed or move gradually upwards without any major pullbacks. 2022 has been a good year for tax-loss harvesting not because the market has delivered, year to date, a lot of losers, but because the market and stocks have spiked violently up and down in a saw-tooth fashion. On the other hand, 2021 was not a particularly fruitful year for tax-loss harvesting, not because there were few losers over the course of the year, but because the market did not experience the large up-swings and pull-backs that create tax-loss harvesting opportunities.

Benefits of Tax-Loss Harvesting

The benefits of tax-loss harvesting are two-fold. There is an immediate benefit of the tax deduction from the realized loss position when it comes to your tax bill – all else being equal, you will pay less capital gains tax on the same market performance. An important secondary benefit is that the tax savings themselves allow you to have more assets invested over time – a compounding effect like re-investing dividends.

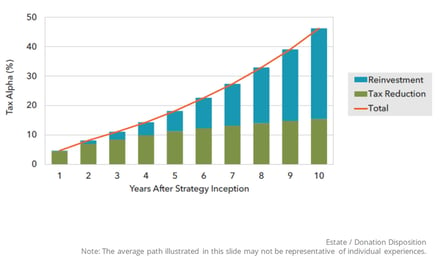

Tax Alpha's 2 Components Both Contribute

Projections Over Time:

Projections Over Time:

- The “tax reduction” component directly reduces the current tax bill by offsetting gains on the Schedule D (1040) with harvested losses

- The “re-investment” component reflects the reinvestment of the tax savings (the tax reduction), which generates additional returns over time (akin to reinvesting dividend)

Tax-Loss Harvesting at BakerAvenue

At BakerAvenue, we conduct tax-loss harvesting across all our strategies throughout the year, and especially towards the year end when the extent of realized gains is more ascertainable.

We also supervise accounts which may be labeled “Active” Tax-Loss Harvesting (Active TLH) accounts. As the name suggests, the number of trades undertaken in an Active TLH account may be many times greater than in our normal strategies. An Active TLH account may be particularly beneficial for those who are anticipating significant capital gains in the future because they have highly appreciated assets that may be sold. These can be:

- Appreciated real estate or personal residence

- Highly appreciated concentrated positions

- Pre-IPO stock

- Sale of a business or exit from a partnership

- Appreciated personal property such as art or collectible

- Deferred gains arising from a 1031 exchange or investment in a Qualified Opportunity Zone

View our Approach to Tax Loss Harvesting

If you or someone you know might benefit from an Active Tax-Loss Harvesting account or have questions regarding tax loss harvesting in general, contact BakerAvenue.