Frequently Asked Questions About the 1031 Exchange and DSTs

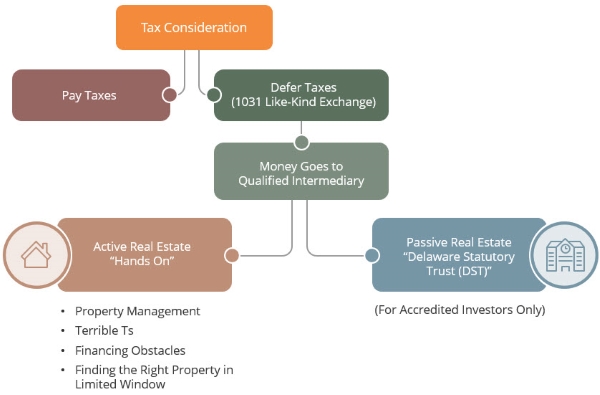

The 1031 exchange offers one of the most strategic planning tools available to real estate investors. A properly executed 1031 exchange can defer taxes, create a sustainable stream of income, and potentially offer estate and liquidity advantages. We can help you strategically maximize the benefits of a 1031 exchange by setting up a Delaware Statutory Trust (DST). With a DST, you can be a part owner of real estate assets by purchasing fractional units and gaining the same benefits as large institutional real estate investors -- without the management hassles.

What is a 1031 exchange?

The tax code has permitted these tax-deferred exchanges of “like-kind” property for many years, most recently reaffirmed under the Tax Cut and Jobs Act passed in 2017[1]. A qualified 1031 exchange allows investors to defer recognition on the gain or loss from a sale of investment or commercial property. 1031 exchanges are not available to sellers of homes that are primary residences. With a 1031 exchange, investors can choose between whole-property purchases and fractionally-owned purchases (i.e., a Delaware Statutory Trust).

Why would I want to set up a 1031 Delaware Statutory Trust (DST)?

While 1031 exchanges can be executed using a Qualified Intermediary (QI), DSTs require additional third-party affiliations. BakerAvenue can provide strategic guidance, planning, access, and the necessary tax considerations for the initial set up. DSTs allow multiple owners to purchase fractional units. The advantages include diversifying and investing in large institutional-style real estate projects to potentially gain the same benefits as larger institutional real estate investors. Another benefit is eliminating the headaches of property management.

What defines "like-kind" property?

If you choose to go with a traditional 1031 exchange, the IRS requires that a property must be “exchanged” for a new property that is the same type. Properties are of like-kind if they’re of the same nature or character (e.g., apartment buildings), even if they differ in grade or quality or are improved or unimproved. They must be held for business or investment purposes and can include apartments, office buildings, shopping centers, storage facilities, land, etc. However, real property in the US is not like-kind to real property outside the US.

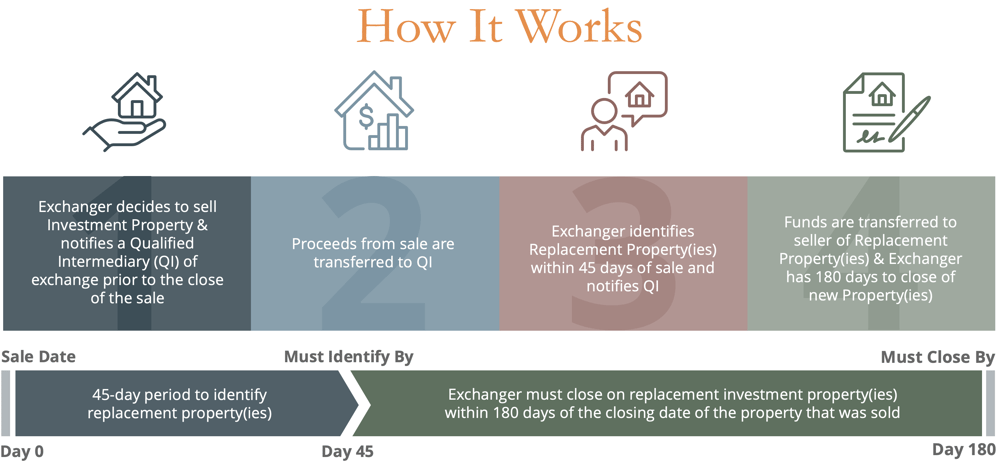

How much time do I have for a 1031 exchange?

45 days.- The identification form requirement is that you need an address of the replacement property by the 45th day of the sale of the original property.

- You should have a firm contract to protect yourself if the potential property is sold to another buyer or unavailable on or after day 46.

Can I change the replacement property?

Yes, but only within the 45 days.- Within 45 days, you can change a potential property, but once the identification period has expired, you cannot substitute or make changes.

- There is no requirement to complete the transaction within 45 days – you must identify the replacement property with specific information.

When must the exchange be completed?

Within 180 days.- The exchange must be completed within the lesser of 180 days from the date of sale of the property being exchanged and the next tax filing.

- This period runs concurrently with the 45-day rule period, so if you wait until day 45 to identify a replacement property, there are only 135 days remaining to complete the transaction.

- There are scenarios where an investor may have less than 180 days, such as tax filing deadlines. The IRS requires that the 1031 exchange be completed prior to filing that year’s taxes. For example, if a property was sold on November 30, the 1031 must be completed by April 15 of the following year. This would create a window of only 136 days.

Deciding What to Do With Your Investment Property

Because the window to complete a 1031 exchange is relatively aggressive, this is where a 1031 in the form of a DST becomes a particularly attractive option. Contact BakerAvenue to determine if a DST is right for you.

Can I get an extension on the time limits?

Only for a state or federally-declared disaster.- If you miss either one of the deadlines, your 1031 exchange will not be valid, and you will be required to pay any capital gains on the sale of your property.

- The IRS doesn’t have provisions for extensions or exceptions – not even to the next business day if the deadline falls on a weekend or holiday – unless there is a state or federally declared-disaster.

- For example, due to the severe storms, flooding, and mudslides that started in January 2023 in California, the IRS issued an extension for the 45-day and 180-day deadlines.

- To get more time, start looking for your replacement property well before closing your sale property or extend the closing date on your sale property.

What is a Qualified Intermediary (QI) and do I need one?

Yes, an intermediary is required unless the exchange is completed on the same day, which is rare.- The intermediary facilitates the exchange by entering into an agreement with the seller of the relinquished property to transfer the property to the buyer and then transfer the replacement property to the investor.

- The QI establishes an escrow account for the proceeds to prevent “constructive receipt” of the proceeds from the sold property. (Constructive receipt requires taxes on income even though money has not been received.)

Can I buy the replacement property first?

Yes, it’s called a “reverse 1031 exchange,” which is more expensive and complex.

Do I just need to reinvest my profit?

No, to defer taxes, you need to replace the entire net sales price of what you sell, not just the gain.- “Net” is the sales price less the closing costs, such as escrow, title, and broker fees.

- Do NOT subtract the loan balance.

Do I have to replace my existing loan amount?

Yes, you need to buy equal to or greater than the entire net sales price to take advantage of the tax deferment.

Do I have to get another loan?

Yes, you need to replace the loan's value with another loan or with additional cash from outside of the exchange.

Do I need to buy the replacement property in the exact same vesting as I sold?

No, but you have to be the same taxpayer.- You can sell the property in your revocable trust and buy it in your name because you are the same taxpayer.

- You can’t sell as a partnership and buy as individuals since those are not the same taxpaying entities.

Can I move into the property I buy?

Yes, but the replacement property needs to be purchased to be a business or investment property.- However, the IRS has safe harbor guidelines (Rev. Proc. 2008-16) that define how to treat your replacement property for the two years after the exchange.

- If you decide to convert for personal property, any conversion should be discussed with your tax advisor.

Can I rent the property to my child or other family members?

Yes, at fair market rent.

Can I buy the replacement property from a related party?

Yes, but there are some very limited exceptions, so you’ll want to speak to your real estate attorney or tax advisor.

.png?width=175&height=175&name=wp-cover-render_Tax-Mitigation%20(1).png) Learn more about Tax Mitigation Strategies When Selling Your Investment Properties and how BakerAvenue can help you navigate through the strategic advantages of exchanges and trusts for your real estate investments. When you need financial advice for your personal and professional life transitions, BakerAvenue is here for you. Schedule your introductory consultation.

Learn more about Tax Mitigation Strategies When Selling Your Investment Properties and how BakerAvenue can help you navigate through the strategic advantages of exchanges and trusts for your real estate investments. When you need financial advice for your personal and professional life transitions, BakerAvenue is here for you. Schedule your introductory consultation.