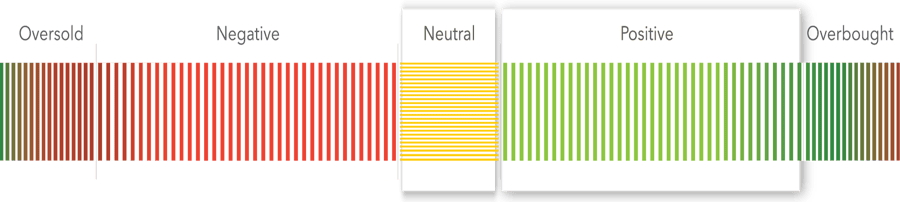

BakerAvenue Prudence Indicator Says...

Long-term: Positive | Short-term: Neutral

Some Tricks, Some Treats

“Wisdom lies neither in fixity nor in change, but in the dialectic between the two.” – Octavio Paz

Volatility has picked up as the debate surrounding fiscal and monetary policy, coupled with stubborn supply chain constraints, raises investor anxiety. Markets were lower in September, with the S&P 500 logging its first decline since January and its worst month in a year. A recovering global economy, together with improving Covid trends, offers a more optimistic outlook. What are the potential tricks, and treats, investors should watch out for as we move deeper into the fall?

The market backdrop has become more complex over the past few weeks. The back half of 2021 always looked more complicated, with global growth set to slow as reopening and fiscal impulses begin to fade, and central banks turn their attention to eventual policy normalization. Recently, the number of risks (tricks) to the status quo has increased. An energy crisis, US politics/debt ceiling, various China worries, supply bottlenecks, slowing growth, more hawkish central banks, and higher interest rates are reintroducing some volatility.

But the treats are there too, and we suspect they are underreported. Demand remains resilient despite supply challenges, with a growing sense that revenues and profits are being held back, not permanently altered, by the logistical challenges. Valuations have improved, with growth rates far surpassing multiple expansions this year. Covid trends are improving, and with it hopes for a more sustained reopening. The sentiment is far from euphoric with trillions in cash and bonds seemingly ready to take advantage of market dips.

From a positioning point of view, it’s been a tale of two markets this year – higher long-term interest rates and the outperformance of cyclicals in the first quarter and again in September, interrupted by lower rates and the outperformance of growth stocks in-between. Nobody said investing was easy! September certainly lived up to its reputation as a tough month with the S&P 500 logging its first decline since January and its worst month in over a year. US stocks outperformed international, growth bested value and large caps outperformed small. Interest rates rose and the commodity complex took another leg higher.

From our perspective, despite evolving tricks and underappreciated treats, the secular bull market remains innocent until proven guilty. We wrote last month that growth rates would start to decelerate as we lap the early days of the pandemic-induced shutdown, and the recovery matures. The move from accelerating growth to decelerating growth is a natural progression of any business cycle, but investors will need to get used to the concept. We also noted the market has yet to fully reflect the above consensus growth we expect in the coming quarters. With trillions still parked in money market funds, it is clear many investors remain under-exposed to that attractive growth setup.

At BakerAvenue, we maintain analytical independence from pre-written market narratives. We remove preconceived biases from the equation and defer to our analytical output. Ultimately, our views are only as optimistic or pessimistic as our technical, fundamental, and macro analyses indicate. Currently, our short-term metrics are in a neutral position. Long-term trends continue to paint a more optimistic picture (positive).

For those who have been following our weekly market updates (view previous market update videos and commentaries), you will be familiar with several of our key concerns and opportunities. For well over a year, we stated that the retrenchment in economic activity in 2020, while necessary, was self-inflicted, not structural, and prone to snapping back as re-opening resumed or vaccines entered the narrative. While we recognize a sustained expansion is quite different than quick normalization, we suspect favorable policy decisions, economic growth, and earnings will continue to support a further grind higher in equities. Consolidations and pullbacks, should they occur during the politically charged weeks ahead, should be bought.

The Fundamental Perspective:

Fundamentally, we continue to focus on the trend in corporate profits and credit metrics. In aggregate, they remain healthy. Our weekly series for forward revenues, earnings, and margins all rose to record highs last month, suggesting that Q3 will also be another record-setting quarter. Earnings season will balance strong demand against pricing pressure and stubborn supply constraints. Net, we expect upside to consensus estimates, but believe the frequency and magnitude of earnings and sales beats will moderate.

Valuations are stretched in some pockets of the market but only slightly above long-term averages in others. The pace of the expansion in corporate profits has exceeded the price pace in stock prices in 2021, so multiples are now lower than they were at the start of the year. Valuation dispersion remains at record levels with a sizable gap between the secular growers and the more economically sensitive recovery plays. We expect less dispersion going forward as investors embrace a more balanced view.

The credit backdrop remains supportive. Both investment-grade and high-yield spreads vs. Treasuries are back to pre-pandemic levels. Because continued tightening here is consistent with a rally in stocks, it has been encouraging to see. Dividend reinstatements (or increases) are now running well ahead of dividend cuts. As corporations’ confidence in their outlook continues to improve, we expect share buybacks and M&A to follow.

The Macro Perspective:

The macro discussion starts with a view on the global economic recovery. Worries have centered on the mix of higher inflation, combined with slowing growth and the beginning of the Fed exit. Stagflation (low growth with elevated inflation) concerns were prominent last month. While it has our attention, we expect the stagflation scare should pass, as conditions generating price spikes ebb (e.g., bottlenecks ease, labor supply increases) and growth picks up.

Interest rates will be the fulcrum by which investors express their economic growth views. We suspect they are somewhat distorted. Low-interest rates, a series of government support packages, a commitment by the Fed, and highly accommodative fiscal policies have buffeted the pandemic shutdowns and laid the groundwork for the recovery. But things are slowly changing on the interest rate front. The Fed recently acknowledged that aggressive bond purchases are not a policy that fits well with a supply-constrained economy. The plan seems to be to taper QE soon (to help address inflation) while holding off on any rate hikes for an extended period (to aid growth). We expect rates to move gradually higher over time as the Federal Reserve pulls back QE and the economy continues to grow.

Regarding the new Delta COVID variant, we are encouraged by the latest readings. Infections and, importantly, hospitalizations are trending lower and should continue to support the recovery trade. It looks as though we are in for an increasingly desynchronized recovery, however, as vaccination rates vary globally. China’s regulatory crackdown will also take its toll. Nevertheless, we continue to expect US GDP growth to be the strongest in forty years.

The Technical Perspective:

The current technical backdrop remains in decent shape. Most major indices remain in well-defined price channels, with shallow pullbacks doing little to alter their longer-term trend. Longer-term moving averages (e.g. the 200-day moving average) remain in good standing with approximately 65% of stocks trading above this key threshold (a healthy level). Shorter-term moving averages (e.g. 50-day moving average) are less convincing and reflect the near-term challenges as only 40% trade above this mark.

Market breadth has improved a bit over the past few weeks, but there is more work to be done as the market remains a bit top-heavy. Currently, the top twenty companies in the S&P 500 make up 42% of its market cap, and the top five a whopping 25%. The “average stock” simply hasn’t kept pace with the largest, predominately technology, issues. We do expect a broadening market as we move into a more seasonally supportive backdrop. October, while historically volatile, often sets the stage for better performance.

Rotation within the market continues to be a weekly theme. Leadership has turned slightly more pro-cyclical of late (e.g. value, small caps, and commodity asset class are picking up relative strength), an encouraging sign. We expect this churning behavior to continue as uncertainty over the pace of the recovery remains. Despite the back-and-forth among asset classes and styles, we were glad to see most major indices continue to hover near all-time highs. Investor sentiment is mixed with money flows into equities picking up, but remaining well below those of bonds and cash. Since 2020, there has been over $2.2 trillion of inflows into bonds and cash vs. roughly $580 billion of inflows into equities (So, four times more inflows into cash and bonds!).

Disclosure: Past performance is not indicative of future performance.