All-Time Highs, Meet the Dog Days of Summer

"There are always flowers for those who want to see them." - Henri Matisse

July closed out six months of positive returns (S&P 500) with several indices reaching all-time highs. Despite the strength, headlines related to COVID variants, China regulations and peak growth pressured the reflation narrative and made for some volatile asset class moves. What should investors expect as we move through the dog days of summer?

July was, in the broadest sense, a “more-of-the-same” month with respect to global equity performance trends in 2021. US large caps led the field and widened their YTD performance gap. Emerging markets underperformed the most but were already in last place after a tough first half of 2021. Everything else fell somewhere in between these extremes. The combination of peaking growth (both economic and earnings-related), the Fed’s more hawkish tone, and risks from the COVID variants have coincided with enough force to shift the narrative and give markets a growth scare.

Large caps outperformed small caps and defensive pockets of the market-led the gains indicating the market has moved towards mid-cycle pricing. Amongst S&P 500 sectors, more cyclically-oriented financials and energy were the only sectors that declined last month. Bond yields moved lower (e.g. the benchmark US 10-year Treasury yield fell 1.2%), and yield curves flattened in risk-off positioning. Real yields dropped further into negative territory. Nevertheless, most equity indices are starting off August at all-time highs. Pullbacks have been short-lived and quickly taken advantage of. Is the defensive positioning signaling something sinister? Should investors care that we are about to move through the hot, sultry days of summer at record price levels?

First, some context. The dog days of summer do have a checkered performance history (e.g. August has the third-worst average monthly return, as well as the third most volatile performance history). To make matters worse, while the S&P 500 has been higher 55% of the time in August, that batting average fell to only 35% following years in which the S&P 500 set one or more new highs in July (there were seven new all-time highs last month). Reasons vary, but a slower pace of business that combines with lighter trading volumes is the go-to explanation.

It is also important to remember each year is unique. We wrote last month that growth rates would start to decelerate as we lap the early days of the pandemic-induced shutdown, and the recovery matures. The move from accelerating growth to decelerating growth is a natural progression of any business cycle, but investors will need to get used to the concept. We also noted the market has yet to fully reflect the above consensus growth we expect in the coming quarters. With trillions still parked in money market funds, it is clear many investors remain under-exposed to that attractive growth setup.

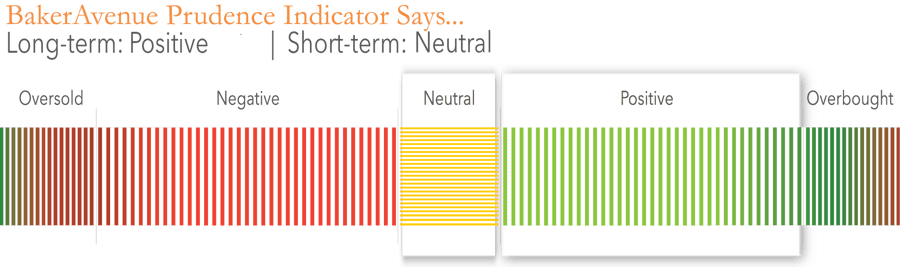

At BakerAvenue, we maintain analytical independence from pre-written market narratives. We remove preconceived biases from the equation and defer to our analytical output. Ultimately, our late Summer views are only as optimistic or pessimistic as our technical, fundamental, and macro analyses indicate. Currently, our short-term metrics are in a neutral position. Long-term trends continue to paint a more optimistic picture (positive).

For those who have been following our weekly market updates (click to view previous market update videos), you will be familiar with several of our key concerns and opportunities. For well over a year, we stated that the retrenchment in economic activity in 2020, while necessary, was self-inflicted, not structural, and prone to snapping back as re-opening resumed or vaccines entered the narrative, read below previous market commentaries. We are seeing that snapback happening now with the economic recovery in full stride. While we recognize a sustained expansion is quite different than quick normalization, we suspect favorable policy decisions, economic growth, and earnings will continue to support a further grind higher inequities. Consolidations and pullbacks, should they occur during these dog days, should be bought.

The Fundamental Perspective:

Fundamentally, we are focusing on the trend in corporate profits and credit metrics. Earnings estimates continue to be revised higher, and we suspect 2021 will end with profit levels at record highs. We run earnings revision screens each week, and in 2021 not a week has gone by where profits weren’t revised higher. The Q2 reporting season is ending on a strong note with record earnings surprises and positive guidance. Supply chain constraints, input cost pressures, and labor shortages are issues we are monitoring and may impact the linearity of upcoming quarters, if just temporarily.

Valuations are stretched in some pockets of the market but only slightly above long-term averages in others. The pace of the expansion in corporate profits has exceeded the price in 2021, so multiples are now lower than they were at the start of the year. Valuation dispersion remains at record levels with a sizable gap between the secular growers and the more economically sensitive recovery plays. During the recent rotation, the growth stocks have benefited most, widening the gap. We expect less dispersion going forward as investors embrace a more balanced view.

The credit backdrop remains supportive. Both investment-grade and high-yield spreads vs. Treasuries are back to pre-pandemic levels. Because continued tightening here is consistent with a rally in stocks, it has been encouraging to see. Dividend reinstatements (or increases) are now running well ahead of dividend cuts. As corporations’ confidence in their outlook continues to improve, we expect share buybacks and M&A to follow.

The Macro Perspective:

The macro discussion starts with a view on the global economic recovery. While it continues, risks remain elevated and concerns we have passed peak growth, particularly in the US, are increasing. A resurgence in COVID cases and uneven vaccine rollout success are leading to an increasingly desynchronized recovery. China's growth remains strong but appears to be slowing as regulatory risks are rising.

Regarding the new Delta COVID variant, we assume that the currently available vaccines are reasonably effective against it. Therefore, even as caseloads rise again, our base case assumes governments will not reinstitute the sorts of lockdowns we saw in 2020, because total hospitalizations will most likely be lower than last year. We continue to expect GDP growth to be the strongest in forty years.

Interest rates will be the fulcrum by which investors express their economic growth views. We suspect they are somewhat distorted. The world’s central banks (e.g. the Fed, the ECB, etc.) have provided the monetary fuel to help boost the recovery. Some reports estimate they are buying more than two-thirds of all Treasury issuance.

Low-interest rates, a series of government support packages, and a commitment by the Fed to highly accommodative fiscal policies have buffeted the pandemic shutdowns and laid the groundwork for the recovery. We expect rates to move gradually higher over time as the Federal Reserve pulls back QE and the economy continues to grow. Inflation expectations have receded over the past month, a welcome sign.

The Fed recently signaled they are beginning to discuss removing some accommodation, but we believe it is still early to be concerned about Fed tightening (rate increases). Despite a more seasoned expansion, we believe investors will see little tightening before late-2022.

The Technical Perspective:

The current technical backdrop remains in decent shape. Most major indices remain in well-defined price channels, with shallow pullbacks doing little to alter their longer-term trend. There have been eight tests of the 50-day moving average (S&P 500) this year; each met with a staunch defense. Longer-term moving averages (e.g. the 200-day moving average) remain in good standing with over 80% of stocks trading above this key threshold (a healthy level).

Internal metrics are a bit mixed. Market breadth has deteriorated slightly over the past few weeks and can be seen by looking at the Value Line index, a great proxy for the average stock (the Value Line Index is an equally-weighted index of approximately 1,500 stocks and is often used to represent the “average” stock). It had a fantastic run into its mid-March peak, strongly outperforming the S&P 500. The last few months haven’t been as kind, with a lot of churning in this relationship. How this tight range resolves itself in the months ahead will say a lot about what the back half holds.

Rotation within the market continues to be a weekly theme. Leadership has turned less risk-on (e.g., IPO/SPACs are performing poorly, volumes are anemic, small caps are lagging recently, etc.), and we suspect that reflects some healthy skepticism. Investor sentiment is mixed with money flows into equities picking up but remaining well below those of bonds and cash. We expect this churning behavior to continue as uncertainty over the pace of the recovery remains. Despite the back-and-forth among asset classes and styles, we were glad to see most major indices continue to hover near all-time highs.

Concluding Thoughts:

In sum, we remain comfortable with our positioning. Volatile Summer months are part of investing and often result in tactical dislocations and opportunities. We have championed a ‘barbell’ approach by investing with secular winners while simultaneously allocating capital toward assets that will benefit most in a recovery. While July rewarded more defensive assets, we feel maintaining some cyclical presence is prudent. Systemic risks that could result in recessionary or bear market conditions remain low given the accompanying growth backdrop. Our forecast for a maturing but sustained economic expansion strengthens our belief that investor focus should be on “how” one is positioned, not “if” they should have exposure at all. That “how” should continue to include both secular growth and cyclical allocations.

Our investment philosophy is based on a dual mandate of growing, and protecting, client assets. With our cash positions now residual in nature, we are focusing on strategy positioning vs. our respective benchmarks to control risk. Should our base case hold, we plan to maintain our steady positioning. Of course, should the backdrop start to destabilize, we will take a more defensive stance.

Given the volatile and ever-changing backdrop, we believe a strategy that combines disciplined fundamental, technical, and macro analyses has the best chance of generating superior risk-adjusted returns. While our forecasts are subject to revision, our commitment to client service is rock solid. Should you have any questions please contact BakerAvenue, we are happy to share our thoughts in greater detail and welcome your questions or comments.