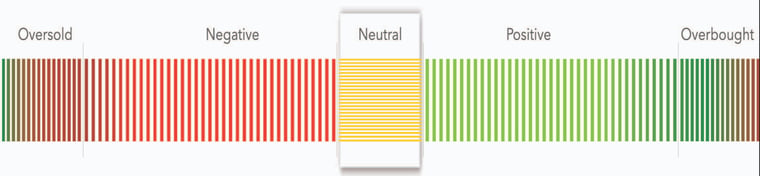

BakerAvenue Prudence Indicator Says...

Long-term: Neutral | Short-term: Neutral

Less Need for Tightening Speed?

“The beginning is the most important part of the work.”

– Plato

Last month we wrote about how the seasonal setup is improving. Right on cue, October turned out to be the S&P 500’s best month this year. Volatile Octobers often set the stage for the market’s best six-month seasonal stretch (e.g., November through April), but we doubt seasonality alone can take credit for the bounce. Investors’ hopes for a “pivot” toward slowing rate hikes grew throughout the month, making the recent Fed meeting an important test. There was something for the bulls and the bears in the announcement, with our main takeaway being there is less need for aggressive rate hikes going forward.

We are calling the latest Fed announcement “pivot-lite,” and therefore incomplete from an explicit signaling perspective. In a well-telegraphed move, the Fed raised its short-term borrowing rate by 0.75 percentage points to a target range of 3.75%-4.00%, the highest level since January 2008. This was the sixth hike of the year and fourth consecutive by 0.75 percentage point increase, continuing the most aggressive pace of monetary policy tightening in over forty years. But the details of the release are where the debate regarding its market impacts starts.

We think it’s right for investors to be focused on any change in Fed policy, a Fed pause has been a bullish stock signal for decades. Markets are forward-looking and work overtime to assess what effects a continuation, or pause, may have on economic growth. And that is where the latest announcement gets interesting. The Fed suggested it will consider “cumulative tightening” and “lags” in the impact of monetary policy while charting its future course for interest rates, a decidedly dovish development. However, they said the terminal rate (the rate at which they end their rate increases) is higher than previously expected, that it is premature to consider pausing, and followed that the window for a soft landing has narrowed, an equally hawkish development.

We feel the Fed built itself an off-ramp from a per meeting rate hike pace. They are signaling they have less need for speed, while simultaneously reminding investors that their steadfast campaign to lower inflation has a way to go. In times like these, it is important to have an investment process in place that removes emotion from the equation. At BakerAvenue, we maintain analytical independence from pre-written market narratives. We remove preconceived biases and defer to our analytical output. Ultimately, our views are only as optimistic or pessimistic as our technical, fundamental, and macro analyses indicate. Currently, both our short-term and long-term metrics are in a balanced (neutral) position.

For those who have been following our market updates (view previous market update videos and commentaries), you will be familiar with several of our key concerns and opportunities. We have continually stated that while growth is slowing, the downturn is more cyclical rather than secular. We do not forecast a break to our longstanding “growth normalization” view.

We do believe volatility will stay elevated, but ultimately, another year of economic and earnings growth should be enough to offset monetary tightening and support an eventual grind higher in equities. While we expect the direst outcomes can be avoided, we acknowledge uncertainty remains. We want to be thoughtful regarding portfolio construction and risk control in these volatile times.

The Fundamental Perspective

Fundamentally, we continue to focus on the trend in corporate profits and credit metrics. Earnings takeaways over the past several weeks have reinforced our belief that, while the growth backdrop remains challenging, there are offsets. Headwinds like dollar strength and input cost pressure are balanced by consumer spending resiliency and improving supply chain commentary. Our weekly series for forward revenues, earnings, and margins have started to move lower, but remain positive on a year-to-date basis. On balance, quarterly results have matched expectations and provided some stalwart defense against any profit-recession narrative. While the frequency and magnitude of earnings and sales beats are normalizing, consensus estimates look beatable, and another double-digit expansion in profits (for ’22) is within reach.

Valuations have corrected and are now below long-term averages. The pace of the expansion in corporate profits has far exceeded stock prices over the past couple of years, so multiples are now well below where they were at this point last year. Valuation dispersion remains high with a sizable gap between the secular growers and the more economically sensitive recovery stocks. Predictably, the backup in rates has caused this dispersion to shrink as the more speculative assets have corrected to a greater degree. We continue to see less dispersion going forward as investors embrace a more balanced view.

The credit backdrop will be important to monitor as growth concerns persist. One of the defining criteria between pronounced or shallow recessions has been the behavior of credit. Both investment-grade and high-yield spreads vs. Treasuries are somewhat elevated but remain at non-recessionary levels. Corporate cash flows remain healthy with dividend reinstatements (or increases) running well ahead of dividend cuts.

The Macro Perspective

The macro discussion must start with a view on the global economy. Incoming economic data continues to support our slowing but not recessionary growth narrative (e.g., employment remains strong, manufacturing reports have stayed in expansionary zones, etc.). GDP growth bounced back to positive territory after two consecutive negative quarters to start the year. Real time estimates show another positive quarter is in store to close out the year. Recent macro worries have centered on the mix of higher inflation, combined with slowing growth and tighter financial conditions (e.g., restrictive monetary policy). While these certainly have our attention, we expect the inflation scare will subside. Cooling input prices (e.g., transportation costs, used car prices, etc.) and easing supply chain pressures amid softening demand and tighter policy suggests inflation momentum has peaked.

Interest rates will be the fulcrum by which investors express their economic growth, inflation, and thus Fed policy, views. Yield curves have inverted as the front end of the curve has moved higher with the prospects of further rate hikes. Curve inversion should be respected, as they have a very strong track record in signaling recession over the past 40+ years. What they cannot predict accurately is the timing of the recession, nor its depth and magnitude. As mentioned, one of the most pressing questions for investors is: Can the Fed get control over inflation without causing a deep recession? It is going to be tricky, but at this point we believe they can.

The Technical Perspective

The technical backdrop remains choppy with the recent action keeping most benchmarks within a volatile trading range over the short term. While still tactically oversold, the range that has defined much of the last several months has still yet to be resolved. For example, the percentage of stocks trading above key moving averages (still low by historical standards) continues to indicate markets are fairly washed out. However, longer-term downtrends remain in place (e.g., most indices are below key moving averages) and volatility has remained elevated. We are on the lookout for sustained stability in these metrics with a more balanced short-term outlook.

Despite the volatility, internal metrics have improved over the past month (e.g., expanding new highs vs. new lows, improving market breadth, etc.). Relative strength in more cyclically oriented pockets of the market is picking up relative strength vs. defensives, an encouraging sign. We expect the market to broaden and leadership to continue to adjust as we move towards the final weeks of 2022. Healthier markets tend to have strong participation rates, so we will be looking for improvement here. Admittingly, we are discouraged by the higher correlations we are seeing within sectors and industries. Lower correlations should come with macro-healing later in the year, and will support a more active approach, an environment we welcome.

Investor sentiment is still quite bearish, which, from a contrarian point of view, is bullish. Surveys (e.g., AAII bull-bear survey, Investors Intelligence surveys, Consumer Sentiment, etc.) point to a skeptical investor base with the number of “bears” still elevated. Tactical positioning data (e.g., put-call ratios, cash balances, etc.) is still leaning defensive and will act as a catalyst should the macro backdrop improve. While not the overriding factor, investor positioning often influences the order of magnitude in market moves (higher, or lower).

Concluding Thoughts

We see little reason to change our outlook considering the Fed’s latest communication. We have championed an active approach of investing with secular winners while simultaneously allocating capital toward assets that will benefit most in a recovery. We do believe the frequency by which investors can actively tilt portfolios towards those pockets of opportunity or away from risk will become more pronounced as growth slows.

Volatility should stay elevated given the macro uncertainties. Systemic risks that could result in prolonged recessionary or bear market conditions exist, but are not overwhelming, given the accompanying growth backdrop. Our forecast for a maturing but sustained economic expansion (i.e., gloomy, yes, but doom, no) strengthens our belief that investor focus should be on “how” one is positioned, not “if” they should have exposure at all.

Our investment philosophy is based on a dual mandate of growing and protecting client assets. We are staying active, using the volatility to harvest losses while opportunistically deploying capital where appropriate. We have lowered our cash weightings and are focusing on strategy positioning vs. our respective benchmarks to control risk. Of course, should the backdrop destabilize, we will take a more defensive stance.

Should you have any questions, please contact BakerAvenue. We are happy to share our thoughts in greater detail and welcome your questions or comments.

Disclosure: Past performance is not indicative of future performance.